The below articles are part of Gorin’s Business Succession Solutions, a complimentary quarterly resource by Thompson Coburn partner Steve Gorin on tax planning for business owners, with an emphasis on income, estate, and related tax considerations. Certain section references in this article correspond to the supporting technical materials included with the publication, which provide additional detail and examples beyond the scope of this article.

To receive future editions of Gorin’s Business Succession Solutions, including access to the full, searchable supporting materials, subscribe here.

Events Triggering § 754 Election

Most estate planners know that, when a partner dies, the partnership can elect under IRC § 754 to pass along to the partnership’s assets the basis step-up in the partnership interest. The following article includes a discussion on:

- Broad ideas of how the § 754 election actually leads to stepping up the partnership’s assets basis (an “inside basis step-up”). See parts II.Q.8.e.iii.(c). When Code § 754 Elections Apply; Mandatory Basis Reductions When Partnership Holds or Distributes Assets with Built-In Losses Greater Than $250,000 and II.Q.8.e.iii.(d). Code § 743(b) Effectuating Code § 754 Basis Adjustment on Transfer of Partnership Interest.

- Events other than death that trigger this step-up, including the adverse Otay Project, LP v. Commissioner, T.C. Memo. 2026-21. See part II.Q.8.e.iii.(b). Transfer of Partnership Interests: Effect on Partnership’s Assets (Code § 754 Election or Required Adjustment for Built-in Loss).

- Strategy when a § 754 election is not timely made, including triggering an event or liquidating the partnership.

From part II.Q.8.e.iii. Inside Basis Step-Up (or Step-Down) Applies to Partnerships and Generally Not C or S Corporations:

See part II.Q.1.g Partnership Basis Adjustments (describing the Code § 755 rules for allocating basis adjustments) and, within this part II.Q.8.e.iii, subparts:

- II.Q.8.e.iii.(a) Illustration of Inside Basis Issue

- II.Q.8.e.iii.(b) Transfer of Partnership Interests: Effect on Partnership’s Assets (Code § 754 Election or Required Adjustment for Built-in Loss)

- II.Q.8.e.iii.(c) When Code § 754 Elections Apply; Mandatory Basis Reductions When Partnership Holds or Distributes Assets with Built-In Losses Greater Than $250,000

- II.Q.8.e.iii.(d) Code § 743(b) Effectuating Code § 754 Basis Adjustment on Transfer of Partnership Interest

- II.Q.8.e.iii.(e) Code § 734 Basis Adjustment Resulting from Distributions, Including Code § 732(d) Requiring an Adjustment Without Making Code § 754 Election

- II.Q.8.e.iii.(f) Code §§ 338(g), 338(h)(10), and 336(e) Exceptions to Lack of Inside Basis Step-Up for Corporations: Election for Deemed Sale of Assets When All Stock Is Sold

- II.Q.8.e.iii.(g) Certain Changes in Inside Basis May Reduce Foreign Tax Credits

When a Code § 754 election is in place and a partner transfers a partnership interest, Code § 743 reconciles the partnership interest’s basis (“outside basis”) against the basis of the partnership’s assets allocated to that partnership interest (“inside basis”). Although one often view the process as applying the outside basis step-up that occurs when a partner dies or the partnership interest is otherwise transferred, the outside basis might have changed relative to the inside basis due to other events, and Code § 743 reconciles the cumulative difference – not just the change in outside basis that triggered this reconciliation. This distinction means that any trigger – not just a basis-changing event – can generate the full basis step-up.

Making the § 754 Election Upon Death: From part II.Q.8.e.iii.(d). Code § 743(b) Effectuating Code § 754 Basis Adjustment on Transfer of Partnership Interest:

Upon a partner’s death (including the death of the grantor of a revocable trust, of the beneficiary of a QTIP trust, or presumably of the holder of a general power of appointment) or on the sale or exchange of a partnership interest, the partnership’s property’s basis is adjusted under Code § 743 if the partnership has in effect a Code § 754 election or makes a Code § 754 election on the partnership tax return that covers the taxable period that includes the date of death, which election might be filed up to 12 months after the due date.

Whether or not a Code § 754 election is in effect, the basis of partnership property is not adjusted as the result of a contribution of property, including money, to the partnership.

The Code § 754 election may not be filed in a year before death occurs, unless some other Code § 743 or 734 event occurs in the year covered by the filing. When a partnership interest is community property and receives an outside basis adjustment of both halves, both halves are eligible for a corresponding inside basis adjustment by reason of that death.

If the basis of the transferee partner’s partnership interest is greater than the former partner’s share of the basis of the partnership’s assets, then the election will give the new partner a stepped-up basis in the partnership assets. This basis adjustment is not necessarily tied to the change in basis between the old and new partner; rather, it is based on the relationship between the outside basis and the inside basis. Of course, a change in basis of the partnership interest affects this relationship. However, prior changes in basis of the partnership also count. In fact, a substituted basis transaction, in which the basis in the partnership interest might or might not change, triggers the basis adjustment; however, no adjustment is made in a substituted basis transaction if the outside basis equals the inside basis. If a partnership does not make a Code § 754 election when a partner dies, consider asking the partnership to make the election when the decedent’s estate or (former) revocable trust funds bequests by distributing the partnership interest, which also might be an event triggering a basis adjustment; as described above, that basis adjustment is not tied to any change in basis but rather generally catches up the “inside basis” to the “outside basis.”

In a sale or exchange situation, the transferee partner’s basis step-up in partnership assets is based on the extent to which the partner’s basis in the partnership interest exceeds the basis of the partner’s share of the partnership’s assets; any contingent payments cause a basis increase to the extent they constitute gain to the seller and potentially deductible interest to the extent they constitute interest income to the seller. If the transfer is caused because of a partner’s death, the basis step-up is based on the fair market value of the deceased partner’s partnership interest as of the date of death, plus the transferee partner’s share of partnership liabilities, minus any allocable income in respect of a decedent items; although liabilities are included in the basis of a partnership interest, they do not generate a basis increase in the partnership’s assets.

A partner’s share of income in respect of a decedent under Code § 691 (IRD) does not receive a basis step-up. Unrealized receivables that constitute IRD are not eligible for a basis step-up.

When a person’s partnership interest is liquidated, the basis of the partnership interest is allocated to the assets that person receives:

- This has led to the observation that, if one is going to liquidate the partnership anyway, a Code § 754 election might not be necessary. However, if the partnership sells its assets and then liquidates, then this strategy might not work as well for state income tax purposes as it does for federal income tax purposes; a Code § 754 election might be particularly important if the owner of the partnership interest resides in a state other than the state in which the partnership does business.

- These rules can generate opportunities to enhance the basis of an asset to be sold (but might be attacked if used to accelerate or duplicate recognition of loss):

- A partner who receives low basis assets can use the basis in his partnership interest to increase the basis in those assets. If a Code § 754 election is not in effect, then this basis increase is not matched by a corresponding decrease in the distributed asset. Absence of a Code § 754 election might or might not be considered abusive in such a case.If a partnership interest with a low basis is liquidated in exchange for high basis assets, a Code § 754 election will take into account the basis reduction in the distributed asset and increase the basis in its remaining assets by a corresponding amount.

The partnership and the transferee partner, including a decedent’s estate, should consider extending their income tax returns so that any IRS adjustments to basis, including the value of assets in the decedent’s gross estate, can be reflected in the transferee partner’s income tax returns; ignoring the interplay of these statutes of limitations can cause the taxpayer to lose the benefit of the basis step-up. For example, suppose decedent died December 1, 2025, and the partnership sold assets December 31, 2025. The estate tax return is due September 1, 2026 (nine months after death) and may be audited as late as September 1, 2029. The estate’s income tax return for calendar year 2025 is due April 15, 2026, and may be amended only as late as April 15, 2029. Thus, audit adjustments on the estate tax return might be made between April 15, 2029 and September 1, 2029, but the estate could not amend its income tax return to reflect any increase in basis due to the audit. The partnership should extend the due date of its return. Additionally, the estate could file an extension for its initial income tax return, so that the return is filed timely by October 15, 2026 (six months being the latest date for an extension). An alternative to extending the estate’s income tax return might be for the estate to choose a fiscal year ending on or after May 31, 2026; note that a Code § 645 election would be required if the decedent’s partnership interest were held in a revocable trust.

If the partnership’s assets are included in the decedent’s gross estate under Code § 2036, the partnership’s assets will receive a basis adjustment, without regard to whether a Code § 754 election was made; any gift of a partnership interest brought back under Code § 2036 qualifies for the new basis, even though the donee and not the donor’s estate owned the partnership interest, and the partnership (and possibly the partners) needs to take appropriate steps to preserve the use of this basis step-up for sales that occur after death and before any estate tax audit concludes. Consider whether an estate that is well below the threshold for paying estate tax would argue that any partnership interest it holds should be disregarded under Code § 2036 and the underlying assets included in the estate, so that the assets could get a higher basis step-up. Query the level of proof required to invoke Code § 2036 in such a situation.

Tiered partnerships may carry the effect of Code § 754 elections throughout the partnership system, if each layer has an election in place. Rev. Ruls. 78-2 and 87-115.

Events Other Than Death That Trigger the Step-Up: From part II.Q.8.e.i. Distribution of Partnership Interests:

Except as otherwise provided in regulations, for purposes of Code § 708 (termination of partnership, which generally no longer applies), Code § 743 (adjustment to inside basis of partnership property when the outside basis of the partnership interest changes), and any partnership income tax matters specified in regulations, any distribution of an interest in a partnership (not otherwise treated as an exchange) is treated as a Code § 761(e) exchange.

Partnership mergers present a particularly instructive context. In TAM 201929019, the IRS addressed an assets-over merger in which partnership X was deemed to contribute all its assets and liabilities to partnership Y, followed by a deemed distribution of Y interests to X’s former partners in liquidation. The IRS concluded that this constructive distribution constituted an exchange under Code § 761(e), triggering a Code § 743(b) adjustment. The taxpayer’s argument that constructive distributions should not trigger Code § 761(e) was rejected.

Not every shift in partnership economics constitutes an exchange, however. CCA 201517006 held that shifting rights to future profits not is treated as a Code § 761(e) exchange; see part II.C.6 Shifting Rights to Future Profits. By contrast, CCA 201726012 adopted a notably broad interpretation, concluding that the regulations do not limit “exchange” to taxable exchanges. Accordingly, a complete liquidation under Code § 332(a) and a reorganization under Code § 368(a) each qualifies as an exchange for Code § 743 purposes, significantly expanding the universe of triggering transactions.

If a partnership does not make a Code § 754 election when a partner dies, consider asking the partnership to make the election when the decedent’s estate or (former) revocable trust funds bequests by distributing the partnership interest, which also might be an event triggering a basis adjustment. The basis adjustment is not tied to any change in basis but rather generally catches up the “inside basis” to the “outside basis,” so every estate or (former) revocable trust has a chance to make up for the partnership’s failure to make a Code § 754 election. Note also that, if a Code § 754 election is in place as of date of death, technically the basis adjustments need to be done not only as of date of death but also as of date of distribution. If the adjustments are made as of date of death and the distribution is a carryover basis event, then the fact that outside basis equals inside basis means that no further Code § 743(b) is required.

However, a disposition of a partnership interest by gift (including assignment to a successor in interest), bequest, or inheritance, or the liquidation of a partnership interest, was not a sale or exchange for purposes of Code § 708. However, the concept of a partnership terminating by reason of a transfer no longer exists. See part II.Q.8.e.iv Transfer of Partnership Interests Resulting in Deemed Termination: Effect on Partnership (repealed by 2017 tax reform).

Code § 761(e)(2) provides, “Except as otherwise provided in regulations, for purposes of … section 743 (relating to optional adjustment to basis of partnership property) …, any distribution of an interest in a partnership (not otherwise treated as an exchange) shall be treated as an exchange.” Regulations do not modify the application of Code § 761(e)(2).

Otay Project LP v. Commissioner, T.C. Memo. 2026-21, disallowed a Code § 743 basis adjustment for lack of substantial economic effect; as an alternative ruling, it also applied the common law economic substance doctrine to hold that certain transactions were a sham; see part II.G.17.c Economic Substance, Sham Transaction, Business Purpose, and Substance Over Form Doctrines. The taxpayer claimed a Code § 743(b) adjustment of approximately $867 million, notwithstanding that the partnership (OPLP) held assets worth only approximately $28 million with liabilities of $71 million. The entity OPLLC—the 99.9% partner of OPLP—reflected negative capital of approximately $912 million.

The court found this calculation illogical. The negative capital defied reality and proper tax accounting: it was fundamentally impossible from a cash perspective for OPLLC to have withdrawn nearly a billion dollars in capital in excess of what it contributed. The discrepancy was attributable to deferred profits under the completed contract method of accounting, and prior distributions of tax-deferred profits had been ignored in the petitioner’s Code § 743(b) calculation. The court held that the claimed adjustment failed to satisfy the requirement of substantial economic effect under Reg. § 1.704-1(b)(2), because OPLLC’s negative capital account carried an unconditional obligation to restore the deficit that was not properly accounted for in the calculation.

As an alternative holding, the court applied the economic substance doctrine to disregard the transactions as a sham. The formation and funding of the so-called Finco entities were inconsistent with the taxpayers’ overall plan for dividing business operations, and the restructuring produced no genuine economic consequences apart from the generation of tax benefits. Despite these severe holdings, the court declined to impose penalties, finding that the taxpayer had obtained a detailed opinion from well-qualified advisors with full knowledge of the facts and had relied on that opinion in good faith.

Strategies for Missed Elections and Preserving Basis: From part II.Q.8.e.iii.(e). Code § 734 Basis Adjustment Resulting from Distributions, Including Code § 732(d) Requiring an Adjustment Without Making Code § 754 Election:

Part II.Q.1.g Partnership Basis Adjustments includes a summary of this part II.Q.8.e.iii.(e) found in the preamble to certain regulations.

In working with the ideas in this part, consider part II.Q.8.a.i.(b) IRS Attacks on Basis Shifting – the Biden administration attempted to expand filing requirements, which the Trump administration reversed.

Special rules apply to unrealized receivables and substantially appreciated inventory items. Also, in reviewing anything in this part II.Q.8.e.iii.(e), consider whether part II.Q.8.e.iii.(g) Certain Changes in Inside Basis May Reduce Foreign Tax Credits may be relevant.

From part II.Q.8.b.i.(e). Basis in Property Distributed from a Partnership; Possible Opportunity to Shift Basis or Possible Loss in Basis When a Partnership Distributes Property:

When the distribution is a liquidating distribution, the partner’s adjusted basis in the distributed property is equal to the adjusted basis of the partner’s interest in the partnership, less any money distributed. Therefore, if a high basis partnership interest is redeemed in exchange for low basis property, the property receives a new basis equal to the basis of the redeemed partnership interest; this basis increase has no consequences to the partnership if a Code § 754 election is not in place (and certain mandatory basis adjustments are not in effect) and no consequences to the redeemed partner or other partners so long as none of the exceptions to the nonrecognition apply. The consequence would be a basis reduction. However, this basis reduction would apply only to the extent of any unrealized losses in the partnership’s assets; it would not reduce the basis of any assets with unrealized gains.

In non-liquidating distributions, the partner’s adjusted basis in the property distributed is simply the partnership’s adjusted basis in the property before the distribution. However, the partner’s adjusted basis in the distributed property cannot exceed partner’s adjusted basis in the partner’s partnership interest less any money distributed at the same time.

The substituted basis portion continues the contributing partner’s depreciation schedule.

If a transferee partner receives a distribution of property from the partnership within two years after acquiring an interest or part thereof in the partnership by a transfer with respect to which a Code § 754 election was not in effect, the partner may elect to treat as the adjusted partnership basis of such property the adjusted basis such property would have as if a Code § 754 election were in effect; see part II.Q.8.e.iii.(e) Code § 734 Basis Adjustment Resulting from Distributions, Including Code § 732(d) Requiring an Adjustment Without Making Code § 754 Election. This applies whether or not the distribution liquidates the partnership interest.

Part II.Q.8.b.i.(g). Code § 751 – Hot Assets describes assets the distributions of which may cause negative consequences.

S Corporation Basis Step-Up Strategies

Unlike the death of a partnership, the death of a person owning S corporation stock does not generate an inside basis step-up. This article will discuss:

- How to replicate an inside basis step-up when the circumstances are right

- How to get assets out of an S corporation to provide some inside basis step-up opportunities

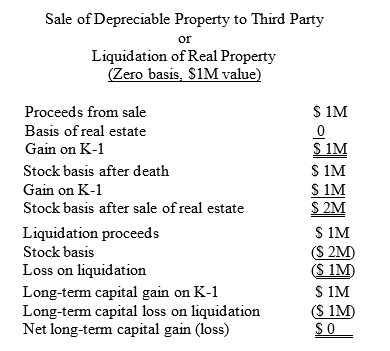

As described in part II.Q.8.e.iii.(a). Illustration of Inside Basis Issue, here is an example of how investing in an S corporation is not as good as investing in a partnership:

An S corporation has assets with zero basis and $1,000,000 value.

Sam Sucker buys 50% of stock for $500,000.

Assets are sold, and S corporation gives Sam a K-1 for his $500,000 share of the gain. Sam is the proud owner of a $1,000,000 basis in his stock ($500,000 purchase price plus $500,000 K-1) that is worth $500,000.

Smart Sally finds a partnership with the same characteristics – assets with zero basis and $1,000,000 value.

Sally buys a 50% partnership interest for $500,000. The partnership makes a Code § 754 election, giving Sally a $500,000 in her half of its assets. When the partnership sells its assets, Sally has no gain on that sale and is content with her $500,000 basis. If assets are not sold, Sally is happy with any depreciation on her share of assets.

Going back to Sam, he does have a way to avoid this terrible result. If the S corporation is liquidated in the same year in which the assets are sold, he can apply his $1 million basis to his $500,000 liquidation proceeds to net a $500,000 loss, which he may be able use to offset gain on the sale of the corporation’s assets. See part II.H.8 Lack of Basis Step-Up for Depreciable or Ordinary Income Property in S Corporation, especially part II.H.8.a.i Solution That Works for Federal Income Tax Purposes (To an Extent). However, if Sam lives in a different state than wherever the assets sale is sourced, then the Sam’s loss on the sale of the stock will not offset the gain on the sale of the assets; see part II.H.8.a.ii State Income Tax Disconnect. Also, to the extent that the S corporation’s assets generated ordinary income on sale, such as recapture of depreciation of personal property, Sam’s capital loss from liquidation will not offset Sam’s ordinary income from the asset sale; see part II.H.8.b Depreciable Personal Property in an S Corporation. Finally, if a substantial part of the S corporation’s assets is sold, but an even larger part is not sold, the other owners are unlikely to be willing to liquidate. Below, let’s delve into these ideas.

Part II.H.8.a.i.(a). Model for Attempting to Replicate an Inside Basis Step-Up provides an example when a decedent owns all of the stock of an S corporation and all of the assets are sold to an unrelated third party, with the corporation liquidating in the same year as the year of the sale:

Although a partner’s share of partnership assets can obtain a basis step-up at that partner’s death, no such relief is available with respect to the assets of a corporation (whether C or S).

Generally, an S corporation can replicate the basis step-up if it holds nondepreciable property in a separate entity, by liquidating after death. That is because the capital gain on the shareholder’s K-1 is offset by a capital loss when the corporation is liquidated. To illustrate, suppose an S corporation holds real estate with zero basis and $1 million value. Decedent owns all of the S corporation. The corporation sells its property to an unrelated third party and liquidates in the year of the sale:

Part II.H.8.a.i.(b). Challenging Issues When S Corporation Liquidates Holding Depreciable Property or Other Ordinary Income Property discusses when this model breaks down. If the property is depreciable and the corporation liquidates, then Code § 1239 might apply to convert the K-1 income to ordinary income. Being a related party transaction might also preclude capital gain treatment given patents in certain situations. Furthermore, if the taxpayer previously sold depreciable property and took an ordinary loss under Code § 1231, gains on the sale of depreciable property will be taxed as ordinary income to the extent of those prior ordinary losses (referred to as Code § 1231 recapture). Finally, the recapture of depreciation deductions taken on personal property constitutes ordinary income under Code § 1245 (see part II.H.8.b Depreciable Personal Property in an S Corporation).

Part II.Q.7.g. Code § 1239: Distributions or Other Dispositions of Depreciable or Amortizable Property (Including Goodwill) explains when Code § 1239 generates ordinary income and how to avoid its application.

Generally, a sale or exchange of property, directly or indirectly, between related persons, will treat as ordinary income any gain recognized to the transferor if such property is depreciable or amortizable property in the hands of the transferee. Also beware similar issues relating to patents.

In this context, “related persons” means:

- a person and all entities which are controlled entities with respect to such person, a taxpayer and any trust in which such taxpayer (or his spouse) is a beneficiary, unless such beneficiary’s interest in the trust is a remote contingent interest, and

- except in the case of a sale or exchange in satisfaction of a pecuniary bequest, an executor of an estate and a beneficiary of such estate.

As used above, “controlled entity” means, with respect to any person:

- a corporation more than 50% of the value of the outstanding stock of which is owned (directly or indirectly) by or for such person,

- a partnership more than 50% of the capital interest or profits interest in which is owned (directly or indirectly) by or for such person, and

- any entity which is a related person to such person under certain attribution rules.

The Code § 267(c) constructive ownership rules apply in determining ownership, including to attribute ownership between individuals who are family members. In addition, stock owned by a trust is considered as being owned proportionately by its beneficiaries.

However, nothing in Code § 267(c) attributes to a trust stock owned by its beneficiaries.

Although stock owned by children would be attributed to each other, that ownership would flow to the trusts. Therefore, even though a corporation would be a controlled entity with respect to each of children, it would not be a controlled entity with respect to any trust owning no more than 50% of the value of its stock.

Therefore, if stock in an S corporation is distributed to separate taxpayer trusts for children after the surviving spouse’s death so that no trust owns more than 50% of the value of its stock, the children’s trusts can liquidate the corporation, and each trust can receive its own property (instead of a tenant-in-common interest in every corporate asset) so it can make its own investment decision separately after the liquidation. Depending on the situation, the trust may need to make an ESBT election.

Returning to Part II.H.8.a.i.(b):

Depreciable property is not the only concern. Consider an S corporation that holds marketable securities. Depending on the nature of a security, its sale might generate ordinary income. For example, if and to the extent that gain on sale of a bond (whether or not the interest is exempt from income tax) results from basis below the bond’s face amount, the gain might be taxed as ordinary income under the market discount rules.

In these cases, the K-1 would include ordinary income, which cannot be offset in any significant measure by the long-term capital loss on liquidation.

With multiple depreciable real properties in an S corporation, one might not be able to sell all the property to a third party in one year, and liquidation would cause this mismatch for the remaining properties. Thus, depreciable real estate should be spun off into a separate S corporation for each property; it’s best to do the spin-off at least five years before death; even then, establishing the required business purpose for a spin-off in real estate might be challenging.

To avoid these complications for an S corporation, and to try to get some benefits for real estate currently held in a C corporation, consider getting the real estate or other assets out of the corporation into an entity taxed as a partnership, as described further below.

From part II.H.8.a.ii. State Income Tax Disconnect:

Suppose the owner of the S corporation lives in a state (the “owner’s state”) that is not the same as the state where the S corporation is domiciled and the property is sold (the “business state”).

Generally, the business state will tax the gain on the sale of the real estate.

However, the owner’s disposition of the S corporation’s stock will not be considered activity in the business state, because generally only the owner’s state can tax the sale of intangible personal property (and stock is intangible personal property).

In the planning stages, taxpayers might try two approaches to avoid this problem, which Consider planning with the following assumptions:

- If one is forming a business entity to hold property in another state, one should consider forming the entity in the owner’s state of residence or in a state that does not impose income tax. Depending on state law, creating domicile in the other state might give it grounds for taxation of certain transactions that might not otherwise exist.

- If the trustee of a nongrantor trust is aware of the need for the planning described in part II.H.8.a Depreciable Real Estate in an S Corporation, consider researching splitting the trust if the trust is in a different state than the business state and the real estate is in one of the states listed above. Note that splitting the trust in this manner would work best if each S corporation owns property in only one state. As mentioned above, depreciable real estate should be spun off into a separate S corporation for each property; it’s best to do the spin-off at least five years before the grantor’s death, even if the trust division does not occur until the sale is contemplated and before any contract is signed.

- If the S corporation formed a new partnership to hold the real estate, then the S corporation might sell its partnership interest and avoid state income tax on the sale of real estate. The partnership would probably not be formed well in advance of the transaction, because the buyer probably would not want to assume the liabilities of an ongoing entity. This in turn might cause step transaction issues at the state level.

From part II.H.8.b. Depreciable Personal Property in an S Corporation:

The disposition of most depreciable personal property, including certain building components depreciated as personal property, will be taxed as ordinary income, whether or not sold to a related party. Thus, all the problems in part II.H.8.a, Depreciable Real Estate in an S Corporation, apply and cannot be avoided for personal property inside an S corporation.

This issue is even more of a concern with current tax laws that allow very quick write-offs on purchases of tangible personal property. Heavy equipment creates a larger concern in that it tends to retain its value for longer.

A solution might be to form a limited partnership that is the original purchaser and leases the equipment to the business. The limited partnership might even borrow from the S corporation at the AFR. When an owner dies, his or her share will receive a new basis if a Code § 754 election is in place. However, the general partner would likely pay self-employment tax on its share of income, and the limited partners might need to pay the 3.8% tax on net investment income – results that would be avoided if the equipment were inside the S corporation. However, navigating these issues to avoid those taxes may be worthwhile, given that the equipment would get an inside basis step-up on a partner’s death.

From part II.H.8.c. Basis Step-Up for Publicly-Traded Stock and Other Nondepreciable Property:

Generally, liquidating an S corporation that holds publicly-traded stock and other nondepreciable property will provide a new basis to its assets by reason of a deemed sale (but perhaps with no taxable income generated), as described in part II.H.8.a.i.(a) Model for Attempting to Replicate an Inside Basis Step-Up, subject to the concerns described in part II.H.8.a.ii State Income Tax Disconnect, but perhaps without the concerns described in part II.H.8.a.i.(b) Challenging Issues When S Corporation Liquidates Holding Depreciable Property or Other Ordinary Income Property.

The corporation could do a formless conversion or merger into an LLC taxed as a disregarded entity or partnership, as described in part II.P.3.a From Corporations to Partnerships and Sole Proprietorships. If the entity is an LLC taxed as a corporation, it might effectuate this change retroactively for two months and 15 days by filing IRS Form 8832.

From part II.H.9. Basis Step-Up In S Corporations That Had Been C Corporations:

An S corporation that used to be a C corporation generate dividend income to its shareholders to the extent that distributions exceed its accumulated adjustments account (AAA). See part II.P.3.b.iv Problem When S Corporation with Earnings & Profits Invests in Municipal Bonds.

A basis step-up does not change this result, even if it results from the S corporation receiving life insurance proceeds. See part II.Q.7.b.iv S Corporation Distributions of, or Redemptions Using, Life Insurance Proceeds.

Furthermore, some redemptions are taxed as distributions, resulting in similar dividend issues.

However, if the S corporation has never been a C corporation or otherwise does not have any C corporation earnings and profits (E&P), these concerns do not arise.

From part II.Q.7.h.iii.(a). Taxable Gain to Corporation When It Distributes Property to Shareholders Other Than in Liquidation of the Corporation:

Code § 311(b)(1) taxes a corporation when it distributes appreciated assets to its shareholders in a distribution described in Code §§ 301-307 (note that corporate liquidations are described in Code §§ 331-346). The corporation is deemed to have sold the assets to the distributee. If the corporation is a C corporation, then the deemed sale is taxed at ordinary income rates, just like any other corporation gain or loss would be. If the corporation is an S corporation, then it is taxed to the shareholders on their K-1s, subject of course to any applicable built-in gain tax under Code § 1374. The entire gain (not just depreciation recapture) from the deemed sale of any depreciable or amortizable property may be taxed as ordinary income (which, in addition to having consequences to S corporation owners, can be an issue to C corporations that have capital losses that could otherwise be offset).

If the distribution is of all of the corporation’s interest in the property, the IRS will attempt to disregard any valuation discounts that would not have applied if the corporation had distributed all of the corporation’s interest in the property to one shareholder. TAM 200443032; Pope & Talbot, Inc. v. Commissioner, 104 T.C. 574 (1995), aff’d 162 F.3d 1236 (9th Cir. 1999).

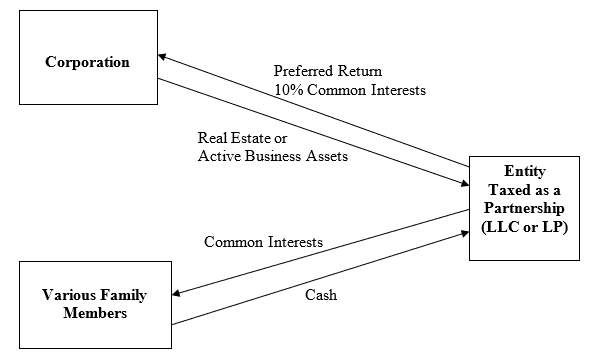

Furthermore, if the IRS determines that a corporation’s receipt of a partnership interest does not constitute adequate and full consideration for the property it transferred to the partnership, the IRS will argue that a dividend was made to the other partners and that the corporation recognized gain on the property deemed distributed to the other partners. TAM 200239001 (property deemed distributed is based on the value of the property contributed to the partnership rather than the value of the partnership interests received by the partner). However, in what might be the same case, the IRS lost that argument, when the taxpayer convinced the court of the taxpayer’s business purpose, in Cox Enterprises, Inc. & Subsidiaries v. Commissioner, T.C. Memo. 2009-134, the application of which is limited by Dynamo Holdings Ltd. Partnership v. Commissioner, T.C. Memo. 2018-61, which enunciated the issue of “constructive distribution.” These cases were a main topic in my 4th quarter 2018 newsletter, which was verbally presented in Planning for Business Exits from C Corporations; Intrafamily Business Transactions; Other Developments. See parts II.Q.7.h.iv. Taxpayer Win in Cox Enterprises When IRS Asserted That Contributing Property to Partnership Constituted Distribution to Shareholders (2009); Dynamo Holdings’ Limitation on Using Cox Enterprises (2018), II.Q.7.h.vi. IRS’ Conservative Roadmap: Letter Ruling 200934013, and II.Q.7.h.vii. What We Learned. Part II.Q.7.h.viii. Value Freeze as Conservative Alternative proposes the following structure:

The corporation contributes the real estate or other business assets to a partnership, taking in return a large preferred partnership interest and an interest in 10% of the residual of the profits (a “common interest”), with the other partners receiving a common interest in the partnership for the balance. Thus, a large majority of the total return (appreciation plus cash flow) that exceeds the preferred interest will be outside of the corporation. Moving to this structure is discussed in part II.E.7.a Overview of How to Migrate into Desired Structure and diagrammed in part II.E.7.c Flowcharts: Migrating Existing Corporation into Preferred Structure, culminating in the above structure, which is shown at part II.E.7.c.ii Moving New LLC into Preferred Structure.

Debt vs. Equity Recent Developments

For many years, C corporations have been using debt created on formation to extract earnings without paying a dividend. Debt is also critically important to intrafamily sales of any type of business entity. This webinar will discuss:

- Regulations on debt vs. equity and the rejection of debt status in Keeton v. Commissioner, T.C. Memo. 2023-35

- When interest on business debt is not deductible, under 2017 tax law changes that were modified in 2025, and opportunities to work around the issue

From part II.G.20.b. When Debt Is Recharacterized as Equity:

Sometimes difficulty arises in determining whether payment obligations constitute debt or equity. For example:

- Once a C corporation becomes profitable, its owners cannot extract earnings generated on their original investment without paying tax. This can come in the form of a dividend or a stock redemption.

- Perhaps one owner contributes capital and the other labor, and they want their entity to be taxed as an S corporation. Because an S corporation cannot have two classes of stock, they need to characterize as the debt the disproportionate contribution of the owner who contributes the capital.

- Sometimes a family member will loan to another to start a business without wanting to receive an equity interest.

The Regulatory Framework of Debt vs. Equity

Congress authorized the promulgation of regulations to distinguish debt from corporate equity generally, but the government did not issue regulations until 2016 or later. Reg. § 1.385-1 sets forth general provisions that are effective for taxable years ending on or after January 19, 2017 and provides rules under Code § 385 to determine the treatment of an interest in a corporation as stock or indebtedness. Reg. § 1.385-3, which addresses certain transactions between related corporations, applies only to certain C corporations. Under these regulations, a “covered member” is defined as a member of an expanded group that is a domestic corporation. The expanded group concept encompasses chains of corporations, other than S corporations, connected through stock ownership.

Thus, Reg. § 1.385-3 applies only to certain C corporations. S corporations and noncovered corporations that issue debt do not need to worry about that regulation and instead look to common law. Key debt-equity Revenue Rulings include 68-54, 73-122, 83-98, 85-119 (limited by Notices 94-47 and 94-48), key excerpts from which are in part II.G.20.b. Various cases set forth multi-part tests for distinguishing debt from equity, including Fin Hay Realty Co. v. United States, 398 F.2d 694 (3rd Cir. 1968), describing typical motivation underlying debt-equity disputes and the resulting tests, and In re Lane, 742 F.2d 1311 (11th Cir. 1984), followed and explained its test used in Estate of Mixon v. United States, 464 F.2d 394, 402 (5th Cir. 1972). Also included are Roth Steel Tube Co. v. Commissioner, 800 F.2d 625 (6th Cir. 1986), cert. denied, 107 S.Ct. 1888 (1987), Hardman v. United States, 827 F.2d 1409 (9th Cir. 1987), Segel v. Commissioner, 89 T.C. 816 (1987), Nestle Holdings Inc. v. Commissioner, T.C. Memo. 1995-441, Pepsico Puerto Rico, Inc. v. Commissioner, T.C. Memo. 2012-269, and Sensenig v. Commissioner, T.C. Memo. 2017-1.

Keeton v. Commissioner, T.C. Memo. 2023-35

Keeton v. Commissioner, T.C. Memo. 2023-35, applied all eleven factors from Hardman to determine whether advances constituted bona fide debt or equity contributions.

Regarding the first factor, the terminology used by the parties, the court noted that no promissory notes were executed during the decade over which advances were made. The contemporaneous documents described the transfers using terms such as “Investment-Idaho Waste” and “capital,” both of which suggest equity rather than debt. A demand note was created in 2008, well after the advances had begun, and the court gave this belated documentation little weight in the analysis.

On the second factor, the existence of a fixed maturity date, the court found that the 2008 demand note contained no fixed repayment schedule. A demand note, standing alone, does not establish the kind of definite repayment obligation that characterizes genuine indebtedness, particularly when paired with the absence of any enforceable timeline for return of the funds.

The third factor, the source of payments and whether the obligor could reasonably be expected to repay, weighed heavily against debt treatment. Over the entire decade, the purported borrower made virtually no interest payments. Only three payments were made, totaling approximately $27,000, against an alleged outstanding balance exceeding $7 million. Furthermore, the borrower carried negative retained earnings of approximately $5.4 million, indicating that the company lacked the financial capacity to service legitimate debt.

Under the fourth factor, whether the lender had the right to enforce payment, the court observed that the purported lender never demanded any security interest in the assets of the purported borrower. This stood in stark contrast to arm’s-length creditors, who demanded and obtained security interests in IWS’s landfill assets as a condition of extending credit. The absence of enforcement rights was a strong indicator of equity.

The fifth factor, participation in management, was treated as neutral.

With respect to the sixth factor, subordination, the court found that the purported loans were subordinated to all outside creditors. The court viewed this subordination pattern as characteristic of equity contributions, not arm’s-length lending. This factor troubles me, in the owner’s loans are always subordinated to outside creditors – a result that would tend to be the case under common law without any special provisions in the documents.

The seventh factor examined objective indicia of debt such as labels used by the parties. As noted above, the internal documents consistently used terms like “investment” and “capital” to describe the transfers, reinforcing the equity characterization.

The eighth factor, thin capitalization, proved devastating to the taxpayer’s position. The debt-to-equity ratio of IWS approached infinity because the company carried liabilities of approximately $12.6 million against negative shareholder equity of approximately $4.4 million. The court viewed a ratio of this magnitude as fundamentally inconsistent with bona fide indebtedness.

On the ninth factor, identity of interest between creditor and shareholder, the court noted that the same families owned 100% of the lender and approximately 69% of the borrower. This degree of overlapping ownership creates an inherent risk that the form of the transaction does not reflect its economic substance.

The tenth factor, the regularity and timing of payments, reinforced the equity characterization. Payments were sporadic and appeared to be tied to earnings rather than any fixed schedule. Virtually no interest was paid over the life of the arrangement.

Finally, under the eleventh factor, the court considered whether the borrower could have obtained comparable financing from an arm’s-length lender. The court concluded that no outside lender would provide more than $7 million on an unsecured basis over a decade at an effective interest rate of zero percent.

Weighing all eleven factors together, the court held that the advances must be recharacterized as equity contributions. Additionally, the court upheld accuracy-related penalties. The return preparer had used a $2 million bad debt deduction figure from IWS’s QuickBooks records on the tax return without conducting any independent investigation into whether the claimed deduction was proper. The case thus serves as a cautionary tale regarding both the substantive debt-versus-equity analysis and the professional responsibilities of return preparers.

Other Cases and Issues

Estate of Fry v. Commissioner, T.C. Memo. 2024-8, allowed a taxpayer to argue substance over form to get basis. In that case, the taxpayer’s profitable S corporation transferred funds to the taxpayer’s loss corporation. The taxpayer failed to document that as a distribution or loan from the profitable company to the shareholder, followed by a contribution or loan from the shareholder to the loss company; however, the court gave the shareholder that favorable treatment anyway. Fry was included in my 4th quarter 2024 newsletter and covered in the related TCLE: Gift Tax Ordinary Course of Business; Proving Basis; Circular 230 Changes.

Stevens v. Commissioner, T.C. Memo. 2025-45, addressed a transaction at issue was structured as a loan combined with an option to purchase property for the outstanding loan balance. Interest was required only when the market rate exceeded a specified threshold, a feature that effectively eliminated any meaningful interest obligation during most economic conditions. The court found that the transaction had no economic effect apart from the generation of tax benefits. The taxpayer claimed millions of dollars in tax deductions that bore no reasonable relationship to the economic outlay. The court imposed a negligence penalty, concluding that the purported tax benefits were, in the court’s characterization, “too good to be true.”

If a debt instrument with a term of more than five years from issuance has original issue discount that exceeds the AFR by more than 5%, the excess may be reclassified as a dividend. Straight debt the term of which was an unknown length between 3 and 9 years was not equity even though its length might be extended to up to 15 years after issuance. Interest on indebtedness of a corporation which is payable in equity of the issuer or a related party or equity held by the issuer (or any related party) in any other person may also be nondeductible.

Although payments made within two years of a partner investing in a partnership generally are presumed to be disguised sales, payments of not more than 150% of the AFR are not presumed to be disguised sales.

See also part II.G.4.a.ii Bad Debt Loss – Must be Bona Fide Debt, II.G.4.d.ii Using Debt to Deduct S Corporation Losses (discussing deducting S corporation losses against loans from shareholders to the corporation and the consequences of doing so), and III.B.1.a.i.(a) Loans Must be Bona Fide.

Deitch v. Commissioner, T.C. Memo. 2022-86, was discussed in my third quarter 2022 newsletter, with the related TCLE Loan Guarantees; Debt in Capital Structure; Ordinary Income on Sale of Business. Along with that I discussed limits on deducting interest.

From part II.G.20.a Code § 163(j) Limitation on Deducting Business Interest Expense:

The business interest deduction helps not only for routine business operations but also for sales of businesses, including sales from a beneficiary spouse to a SLAT created for his or her benefit. As described in part III.B.6.d Divorce as an Opportunity to Transfer, including Code § 2516; Code § 1041 Exclusion for Sales between Spouses, Code § 1041 prevents recognition on gain from sales between spouses but does not prevent recognition of interest income and expense arising from that sale. Business interest expense is reported on Form 1040, Schedule E, Part 2, which means that – mechanically – it is deducted in arriving at gross income.

Generally, Code § 163(j) business interest expense is limited to 30% of “adjusted taxable income.” As discussed in my second quarter newsletter, which was verbally presented in the related TCLE, eliminating the depreciation deduction from “adjusted taxable income” is a huge benefit, especially now that bonus depreciation is permanent.

Small businesses are not subject to this rule. The business’ average annual gross receipts of such entity for the 3-taxable-year period ending with the taxable year which precedes the taxable year cannot exceed $25 million, indexed for inflation ($32 million for 2026), with related businesses aggregated and various other qualifications. Businesses that generate losses might not be eligible for this exception.

Electing real property trade or business, electing farming business, and certain utilities and energy businesses are exempt from the Code § 163(j) limitation. Floor plan financing indebtedness – related to a motor vehicle inventory – is not subject to the Code § 163(j) limitation.

If interest to buy ownership in a business is classified as investment interest under Code § 163(d), the deduction is limited to the taxpayer’s net investment income; “net investment income” here is very different in scope than the idea in part II.I 3.8% Tax on Excess Net Investment Income (NII). Investment interest is an itemized deduction and therefore subject to the 2/37 disallowance described in part II.G.4.n.i.(b) Code § 68 “Pease” Limitation on Itemized Deductions, which is found in part II.G.4.n.i Itemized Deductions.

To the extent practical, try to convert any sale of a partnership interest to a redemption under Code § 736: to avoid paying interest on tax deferred under the installment method, to permit basis to be applied first instead of pro-rated, to permit basis step-up instead of locking in income in respect of a decedent, and to avoid the above limitations on deducting interest income (given that the interest component can be expressed in terms of a Code § 736(a)(1) preferred profits interest). See part II.Q.8.b.ii.(d) Comparing Code § 736(b) to an Installment Sale.

Upcoming Events

Steve Gorin has several upcoming speaking engagements and educational offerings focused on estate, trust, and tax planning. In May, he will present at the NYCPA Estate Planning Conference on the use of nongrantor trusts to hold partnership interests, speaking alongside TC counsel Lisa Bordoff Procopio from the firm’s New York office.

Looking ahead to 2026, Steve will participate in the Minnesota Probate and Trust Law Section Conference, where he will cover planning with life insurance LLCs in light of Connelly and Huffman, and he will also serve on a panel for the 2026 Tax Law Update. In addition to these live events, Steve continues to offer free quarterly webinars that qualify for CPE credit through his relationship with CPA Academy; interested professionals are encouraged to check his CPA Academy webpage regularly for newly posted webinars and CPE opportunities.

Upcoming events and registration details:

- NYCPA Estate Planning Conference

Using Nongrantor Trusts to Hold Partnership Interests

May 21 – Register via the Estate Planning Conference

Co-presenting with Lisa Bordoff Procopio (TC counsel, New York) - Minnesota 2026 Probate and Trust Law Section Conference

Planning with Life Insurance LLCs after Connelly and Huffman

2026 Tax Law Update, Panelist

June 8 – Register at: https://www.minncle.org/seminar/1051792601 - Free Quarterly Webinars (CPE Eligible)

Offered through CPA Academy

Visit Steve’s CPA Academy webpage monthly for the latest webinar links and CPE information

Save the Date!

Join Steve on July 28, 2026 for a webinar discussing the Second Quarter 2026 newsletter.